Pharma stock jumps 12% after reporting ₹82 Cr profit from loss of ₹108 Cr QoQ

ITC (NS:ITC) has been testing the patience of the investors for almost a decade now. ITC is the second largest FMCG company after Hindustan Unilever (NS:HLL) Limited (HUL) in terms of market capitalization, it also has great free cash flow abilities, and it is one of the undervalued stocks in the FMCG sector when compared to its competitors. Yet it has underperformed the Sensex by almost 5.1% in the last 10 years and by 32% in just the last year. Its price has hardly moved in the last 5 years.

Five Sectors of ITC

Cigarettes Business

ITC's cigarette business has been a consistent revenue generator in the past, and it will continue to be so in the future.

In India, there are over 27 crore people who use tobacco products. Cigarette and beedi consumers account for 10 crores of the total. Beedi is used by 80% of the consumers, while cigarettes are used by the remaining 20%. Beedi is a kind of unorganized off-market. This implies that there is a lot of room for the company to expand its cigarette business.

FMCG – Others Business

FMCG-Others is the next main business for ITC. The contribution of FMCG – Other business verticals to revenue is quite healthy. Between April 2020 and December 2020, the company launched over 100 products in the hygiene and natural categories in response to the rising demand for staple and packaged food products. Hygiene products account for 5% of FMCG revenue, and their e-commerce sales have doubled year on year.

3rd party Ad. Not an offer or recommendation by Investing.com. See disclosure here or remove ads.

Hotel Business

The company's hotel business continues to be a loss-making segment. Their revenue contribution dropped from 4.3 percent in Q3FY20 to 1.8 percent in Q3FY21. The pandemic has been an added disadvantage for them.

Agri-Business

ITC sources the finest Indian Feed Ingredients, Food Grains, etc… and is one of the country's largest exporters of Agri products. Agri-Business generated 18.7% of total revenue, with wheat supplies for Ashirwad Atta accounting for the majority, as well as trading opportunities for Rice, Soya, and Wheat.

Paperboard, Papers & Packaging Business

ITC manufactures cigarette papers and components, FMCG cartons, electrical insulation papers, Bio-based Barrier Coated Board, writing and printing papers, etc...This business vertical's contribution to revenue mix has decreased by 0.9 percent year over year.

Top 4 reasons why ITC prices are just not moving

High dependence on Cigarette business

ITC sold cigarettes for almost six decades until the company decided in the mid-1970s that it was time to expand and branch out into new territories. But to this day, ITC is known for tobacco.

The tobacco industry works in a little different way. They can’t market and advertise the product as per their liking. They can't package it however they want. If they truly want to establish a power base, they will need a great distribution network that can reach every part of the country.

3rd party Ad. Not an offer or recommendation by Investing.com. See disclosure here or remove ads.

ITC is a well-known brand for cigarettes. They have an unparalleled distribution network. In the organized sector, ITC has an 84 percent market share which is close to monopoly territory.

The only real danger is posed by the government's tax policy. Cigarettes are tagged as sin products. The government can highly tax them. In the past 5 years, the taxes on Cigarettes have increased from 45% to 56%.

ITC can pass the increase in the tax to the customer. Customers who smoke compulsively are difficult to get rid of. They'll pay a premium and continue to smoke. But if they push them too far, the smokers will be forced to make some difficult decisions. They might switch to a different brand or different tobacco product, or they might start using illegal Cigarettes.

In the below chart we can see the increase in the volume of consumption of illegal Cigarettes as the taxes have increased over the years. So, this has affected ITC which operates in the organized sector. As a result, smokers have options, and a slanted tax system can have a visible impact on a company's profits.

Excessive Diversification and pain of hotel business

ITC is into a large array of industries that are not related to each other.

Luxury hotels are not like cigarette companies. This is a very seasonal business and serves a small number of people. Even if the hotels are empty, they must still cover fixed costs, maintenance costs, licensing fees, and pay salaries. The economics of running a luxury hotel chain is not so great, ITC barely makes a 3% return on all of the capital they've invested in it.

3rd party Ad. Not an offer or recommendation by Investing.com. See disclosure here or remove ads.

Luxury hotels are low ROCE (return on capital employed) business whereas Cigarettes are high ROCE business. Therefore, moving the capital from high ROCE business to low ROCE business like Luxury Hotels, B2B Agriculture products, and Information technology does not make good money management moves.

This affects the overall profitability and the margins of ITC.

The Hope that non-cigarettes FMCG will grow

ITC experimented with edible oils and financial services. However, these ventures had failed even before they took off.

The FMCG business in general has high P/E ratios, zero debt, and a lot of free cash flow and high margins because their brands are very strong.

The below chart shows how Nifty FMCG has performed well when compared to NIFTY Index in the past 5 years.

In the mid-2000s, ITC made a splash by taking on every FMCG product category. With their line of personal care products, they began competing with HUL and P&G. With their line of biscuits, they began competing with Britannia (NS:BRIT) and Parle-G. They even set foot into instant noodles and confectioneries to compete with Nestle (NS:NEST).

ITC’s FMCG segment's revenues increased from 500 crores in 2005 to 13,000 crores in 2020, but profitability remained a concern.

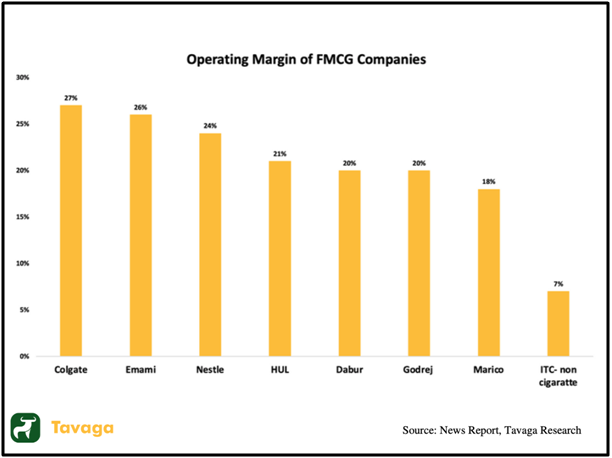

Some of its peers have margins of 15-20%, but ITC has margins of about 2-3%. Even though the FMCG business accounts for a quarter of ITC's total revenue, it only accounts for 3% of the company's profits.

3rd party Ad. Not an offer or recommendation by Investing.com. See disclosure here or remove ads.

One of the biggest reasons is the product portfolio. 30% of products fall in categories that cannot have high margins. Example: - Ashirwad wheat flour, Bingo chips, Yippee noodles.

Another reason is, ITC has always wanted to build its products and brands rather than relying on acquisitions. The process of establishing a brand takes time. So, even though ITC tries to compete with their peers by aggressively pricing their products, they still have higher costs because they're a late entrant in this market.

Shadow over ESG compliance

Institutional investors place a high value on environmental, social, and governance (ESG) factors. If the company's activity or product is harmed by the environment, the company is marked negatively. Cigarettes are to blame in the case of ITC. Cigarette smoking has an impact on other people on a social level as well. But ITC has never had any governance issues.

ITC's cigarette business, which accounts for roughly 85% of its earnings before interest and taxes in FY20 (EBIT) has been hit hard by ESG concerns in recent years, resulting in a drop in price-to-earnings multiples. The company has been emphasizing to investors that it has some ESG offsetting factors, such as being water positive for 18 years, carbon positive for 15 years, and solid waste recycling positive for 13 years. But the investors are not very satisfied with these offsetting factors.

To compensate for the type of business it operates in, a company like ITC must do even better on the ESG score.

3rd party Ad. Not an offer or recommendation by Investing.com. See disclosure here or remove ads.

ITC and its Dividends

In the meantime, they're having trouble keeping up with the influx of cash. They already distribute 85 percent of their profits to shareholders in the form of dividends. The company has a cash balance of 25,000 crores on its balance sheet. It also generated free cash flows of Rs 11,700 crores (FY20). They have an issue with having too much money. Yes, this is a problem because investors are unsure what ITC will do with the money.

ITC and Trolling

ITC was Indian Twitter's favourite punching bag when its stock fell from 204 to 163 a share between August 2020 and October 2020. Most of the market was recovering from the March 2020 fall but ITC continued to fall, adding fire for more trolling of the company. ITC shares have fallen at an annual average of 14 percent in the last 3 years. The company management has also been blamed for poor capital allocation. But also, on another hand domestic mutual funds have doubled their holdings in the stock. However, ITC has recovered pretty well in the previous few months.

What events should investors look forward to?

Demerger of non-cigarette FMCG business and cigarette FMCG business into separate entities. This will unlock a massive value of the cigarette selling business. This will help in improving their margins and profitability.

Selling their non-core and non-profitable business. If ITC decided to sell its nonperforming assets like the hotel business, there will be huge value unlocking and also massive capital inflow which they can allocate to better business.

3rd party Ad. Not an offer or recommendation by Investing.com. See disclosure here or remove ads.

Managements of ITC have been working for a long period. A change in management will add a new perspective to the business and an outsider perspective could add better value to the business.

Which stock should you buy in your very next trade?

AI computing powers are changing the stock market. Investing.com's ProPicks AI includes dozens of winning stock portfolios chosen by our advanced AI.

Year to date, 3 out of 4 global portfolios are beating their benchmark indexes, with 98% in the green. Our flagship Tech Titans strategy doubled the S&P 500 within 18 months, including notable winners like Super Micro Computer (+185%) and AppLovin (+157%).

Which stock will be the next to soar?